Property has long held a special place in the minds of UK investors. In recent years, interest in property investment has remained strong, with many viewing bricks and mortar as a reliable way to build wealth alongside other investments.

The tangible nature of property, combined with the potential for rental income and long-term capital growth, makes it an attractive option for many. However, the experience of owning property extends far beyond the purchase price and projected returns.

Whether you're building wealth during your working years, approaching retirement, or planning for greater financial independence, understanding the broader implications of property ownership can help you make informed long-term decisions.

Successful financial planning is about more than selecting investments with attractive returns. Different assets place varying demands on your finances, time and attention, all of which can influence the role they play within your overall plan.

In this blog, I'll explore some of the wider considerations of property ownership. By understanding both the financial and practical aspects, you can review how your resources are allocated and whether a particular investment aligns with your long-term goals.

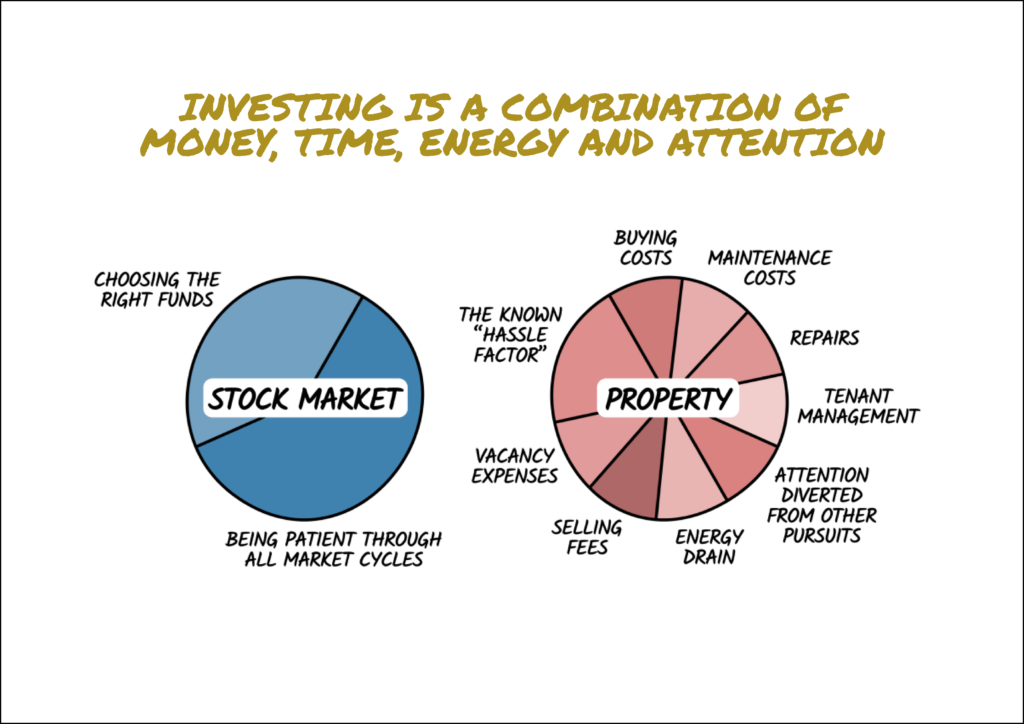

To illustrate these considerations, we'll compare two asset classes that remain popular with investors: equities (ownership in businesses through shares and funds) and residential property.

Owning a diversified portfolio of equities requires careful planning and an investment strategy that aligns with your objectives. Once established, however, a well-structured portfolio can often require relatively little day-to-day involvement.

Periodic reviews help ensure that your investments remain appropriate for your circumstances and goals. The underlying companies are managed by experienced leadership teams, while investment funds are often overseen by proficient managers and chosen/evaluated by financial planners.

There are, of course, costs associated with investing, including fund charges and professional advice. Even so, these costs should always be weighed against the value of receiving expert guidance and maintaining a disciplined investment approach.

One of the key challenges of equity investing is coping with short-term market fluctuations. Investment values can rise and fall, sometimes significantly, and remaining focused, resisting knee-jerk decisions, can require patience and discipline. For many investors, maintaining perspective during periods of market volatility is an important part of achieving their long-term goals.

Property ownership can provide attractive benefits, including the potential for rental income and capital appreciation. Yet, it often involves a broader range of responsibilities and costs than may initially be apparent.

Alongside acquisition costs, investors may need to account for maintenance, insurance, financing costs, taxation, periods without tenants, property management fees and unexpected repairs. These expenses can have a meaningful impact on overall returns and should form part of any investment assessment.

Owning and managing property can also require a greater degree of ongoing involvement. Whether managed personally or through an agent, decisions relating to tenants, maintenance and regulatory requirements often demand time and attention.

For some investors, these responsibilities are a worthwhile trade-off. For others, particularly those looking ahead to retirement or seeking a more hands-off approach to managing their wealth, the practical demands of property ownership may be less appealing.

Liquidity is another important consideration. Unlike many investment portfolios, property cannot usually be sold in stages. Accessing capital often requires the sale of the entire asset, which can make financial planning less flexible and may create additional costs associated with valuation, legal work and the sale process.

These factors do not make property a poor investment, but they do highlight the importance of considering the full picture before committing capital.

Property can be an effective component of a long-term investment strategy. Equally, diversified equity investments may offer advantages that appeal to investors seeking simplicity, flexibility and a lower level of ongoing involvement.

The most appropriate approach will depend on an individual's objectives, circumstances, preferences and tolerance for risk.

Effective financial planning involves more than comparing expected returns. It requires careful consideration of how different investments fit into your life, the commitments they require and the role they play in supporting your long-term goals.

As you review your investment strategy, it can be helpful to consider not only the financial characteristics of each asset, but also the time, energy and attention needed to manage it. Taking a broader view can help ensure that your investment decisions support both your financial wellbeing and your desired lifestyle.

The value of investments and any income can go down as well as up and cannot be guaranteed.

This content is for information purposes and should not be treated as financial advice. We would always recommend speaking to a professional before making decisions regarding your wealth. The information contained in this blog post is based on 2plan wealth management Ltd’s current understanding of tax laws as at April 2026. These laws are subject to change at any time and 2plan wealth management Ltd cannot be held responsible for any decisions made as a result of this newsletter. Tax advice is not regulated by the Financial Conduct Authority

.